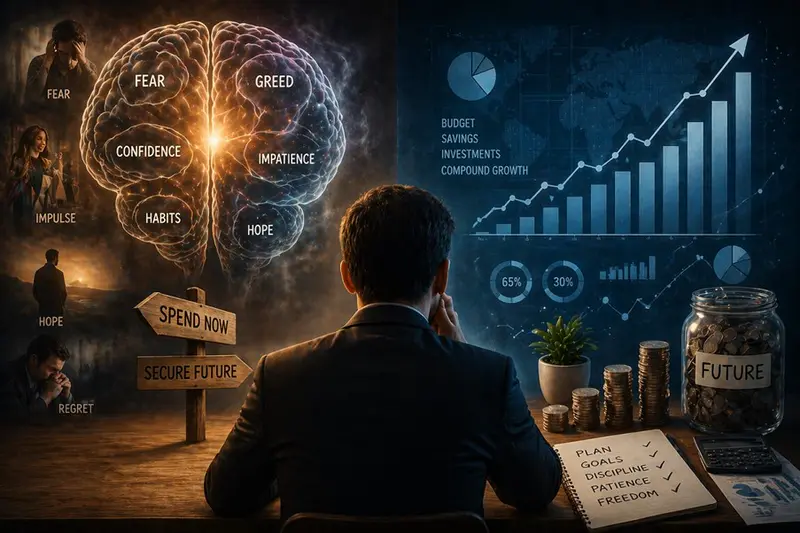

The Psychology of Money—Why Financial Decisions Are Rarely What They Seem

Money is often seen as a numbers game.

Budgets, interest rates, returns, and financial plans—these are the tools people rely on to manage their finances. On the surface, it all appears logical and structured, driven by calculations and careful decision-making.

But beneath that surface lies something far more complex.

Because when it comes to money, people don’t always act logically.

They act emotionally.

They react to uncertainty, habits, fear, optimism, and even subtle influences they may not fully recognize. And these hidden drivers are quietly shaping financial behavior in ways that go far beyond spreadsheets and strategies.

Welcome to the psychology of money—a force that influences nearly every financial decision we make.

Why Money Is Not Just About Math

Traditional financial thinking assumes that people make rational decisions.

They evaluate risks, compare options, and choose what is most beneficial.

In reality, this is rarely the case.

Behavioral finance—a field that studies how psychology influences financial decisions—shows that individuals are often affected by biases, emotions, and mental shortcuts (Wikipedia).

This means:

- People may spend impulsively

- Avoid risks even when opportunities are strong

- Hold onto investments longer than they should

These behaviors are not mistakes—they are human tendencies.

And they are surprisingly consistent across individuals and markets.

The Hidden Role of Emotions in Financial Choices

Every financial decision carries an emotional component.

Fear can lead to caution.

Excitement can lead to risk-taking.

Uncertainty can lead to hesitation.

These emotional responses influence how people:

- Spend money

- Save money

- Invest money

For example, during periods of economic uncertainty, many individuals shift toward more cautious financial behavior—prioritizing savings and essential spending.

Recent insights show that consumers are increasingly balancing caution with optimism, adjusting spending habits while exploring new financial tools and solutions (GWI).

This reflects a deeper truth:

Financial decisions are not just about what people can do—they are about what people feel comfortable doing.

The Rise of Financial Awareness

In recent years, there has been a noticeable shift in how people approach money.

More individuals are:

- Tracking their spending

- Setting budgets

- Focusing on financial stability

Data shows that over half of consumers now actively use budgeting strategies to manage their finances, reflecting a growing awareness of financial habits (YouGov).

This shift is not driven by complexity—it is driven by clarity.

People want to understand where their money goes and how to control it.

And that desire for control is deeply psychological.

Why Habits Matter More Than Plans

Financial success is often associated with long-term planning.

But in practice, habits play a much larger role.

Small, repeated actions—such as saving regularly or monitoring expenses—have a greater impact than occasional big decisions.

This is because habits:

- Reduce the need for constant decision-making

- Create consistency

- Build momentum over time

Behavioral studies suggest that consistent financial behaviors are more effective than relying on motivation alone.

In simple terms:

What people do every day matters more than what they plan to do someday.

The Influence of Perception on Value

Another important factor in financial behavior is perception.

People do not always evaluate value objectively.

Instead, they rely on how something feels.

For example:

- A discount may feel like a gain—even if the purchase is unnecessary

- A price increase may feel significant—even if it is small

- A familiar brand may feel more valuable—even without clear differences

These perceptions influence spending decisions in subtle ways.

They shape not just what people buy—but how they justify those decisions.

Technology Is Amplifying Financial Behavior

Modern technology is playing a growing role in shaping financial decisions.

Digital platforms, mobile apps, and AI-driven tools are making financial management more accessible.

They allow individuals to:

- Track spending in real time

- Receive personalized insights

- Automate financial tasks

At the same time, technology is influencing behavior.

It simplifies decision-making, reduces friction, and encourages engagement.

As a result, people are more connected to their finances than ever before.

But this also means their behavior is being shaped continuously—often without conscious awareness.

The Balance Between Control and Convenience

One of the most interesting trends in finance today is the balance between control and convenience.

People want:

- Greater control over their finances

- Simpler, more convenient tools

This creates a dual expectation:

- Transparency in financial decisions

- Ease in financial management

Organizations that understand this balance are better positioned to meet evolving consumer needs.

Because financial behavior is not just about outcomes—it is about experience.

Why Financial Behavior Is Changing Now

Several factors are contributing to changes in financial behavior:

- Increased access to information

- Greater economic awareness

- Advancements in financial technology

- Shifting consumer expectations

At the same time, financial well-being indicators are improving, with many individuals feeling more confident about their savings and ability to manage expenses (Deloitte Italia).

This combination of awareness and confidence is reshaping how people approach money.

It is creating a more engaged—and more thoughtful—financial mindset.

The Gap Between Knowledge and Action

Despite increased awareness, there is often a gap between what people know and what they do.

For example:

- People understand the importance of saving—but may delay it

- They recognize the value of budgeting—but don’t always follow through

- They are aware of financial risks—but may still take them

This gap exists because knowledge alone is not enough.

Behavior is influenced by:

- Emotions

- Habits

- Context

Understanding this gap is key to improving financial outcomes.

Why This Matters for Businesses

For businesses, understanding financial behavior is essential.

It helps them:

- Design better financial products

- Improve customer engagement

- Build trust and long-term relationships

Organizations that recognize the psychological side of finance can create solutions that align with how people actually behave—not just how they are expected to behave.

This leads to better outcomes for both businesses and consumers.

A More Human View of Finance

The biggest shift in finance today is not technological—it is conceptual.

Finance is no longer viewed purely as a system of numbers.

It is understood as a system of behavior.

This means:

- Decisions are influenced by psychology

- Outcomes are shaped by habits

- Success depends on consistency

It is a more human way of understanding money.

Final Thoughts: The Decisions Behind the Numbers

Money may be measured in numbers.

But the decisions behind it are human.

They are influenced by emotion, shaped by habits, and guided by perception.

Understanding this changes how we think about finance.

It moves the focus from calculations to behavior—from what people should do to what they actually do.

And perhaps the most important realization is this:

Financial success is not just about making the right decisions.

It is about understanding the forces that shape those decisions in the first place.